CALIFORNIA HOMEOWNER BILL OF RIGHTS

Kamala D. Harris, Attorney General of California

The 2012 California Homeowner Bill of Rights is a legislative package designed to bring fairness, accountability and transparency to the state’s mortgage and foreclosure process.

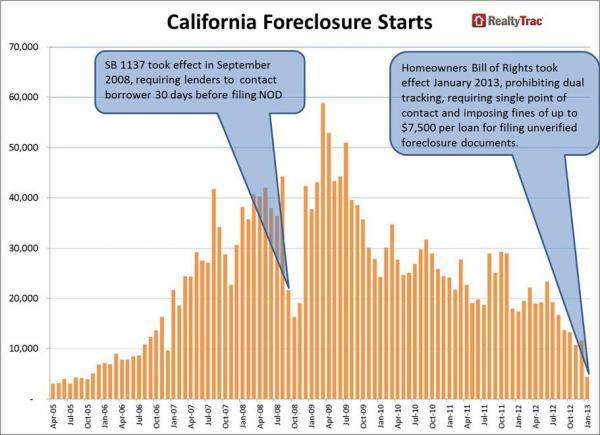

More than one million California homes were lost to foreclosure between 2008 and 2011—with an additional 500,000 currently in the foreclosure pipeline. Seven of the nation’s 10 hardest-hit cities by foreclosure rate in 2011 were in California.

The California Homeowner Bill of Rights marks the third step in Attorney General Harris’ response to the state’s foreclosure and mortgage crisis. The first step was to create the Mortgage Fraud Strike Force, which has been investigating and prosecuting misconduct at all stages of the mortgage process. The second step was to extract a commitment from the nation’s five largest banks of an estimated $18 billion for California borrowers. The settlement contained thoughtful reforms but are only applicable for three years, and only to loans serviced by the settling banks.

Two key bills contain significant mortgage and foreclosure reforms. AB 278 (Eng/Feuer/Mitchell/Pérez) and SB 900 (Leno/Evans/Corbett/DeSaulnier/Pavley/Steinberg) have been thoroughly considered by a legislative conference committee. The major provisions of the bills include:

Dual track foreclosure ban – The legislation would require a mortgage servicer to render a decision on a loan modification application before advancing the foreclosure process by filing a notice of default or notice of sale, or by conducting a trustee’s sale. The foreclosure process is essentially paused upon the completion of a loan modification application for the duration of the lender’s review of that application.

Single point of contact – The legislation would require a mortgage servicer to designate a “single point of contact” for borrowers who are potentially eligible for a federal or proprietary loan modification application. The single point of contact is an individual or team which must have knowledge of the borrower’s status and foreclosure prevention alternatives, access to decision makers, and the responsibility to coordinate the flow of documentation between borrower and mortgage servicer.

Enforceability – Includes authority for borrowers to seek redress of “material” violations of the legislation. Injunctive relief would be available prior to a foreclosure sale and recovery of damages would be available following a sale.

Verification of documents – The legislation would subject the recording and filing of multiple unverified documents to a civil penalty of up to $7,500 per loan in an action brought by a civil prosecutor. It would also allow enforcement under a violator’s licensing statute by the Department of Corporations, Department of Real Estate or Department of Financial Institutions.

v v v v

The other bills in the California Homeowner Bill of Rights are:

BLIGHT PREVENTION LEGISLATION: AB 2314 (Carter) & SB 1472 (Pavley and DeSaulnier) to help combat the blight and crime associated with foreclosed properties.

v AB 2314: Passed out of Assembly (71-0). It was passed out of Senate Judiciary on June 26 (4-0). It will be heard next on the Senate floor.

v SB 1472: Passed out of Senate (36-0). It passed out of Assembly Housing and Community Development (7-0) on June 27, and will be heard next in Assembly Judiciary Committee on July 3.

TENANT PROTECTION LEGISLATION: AB 2610 (Skinner) and SB 1473 (Hancock) to help protect tenants in foreclosed properties.

v AB 2610: Passed out of Assembly (56-14). It will be heard next in Senate Judiciary on July 3.

v SB 1473: Passed out of Senate (25-13). It passed out the Assembly Housing and Community Development on June 27 (6-1) and will be heard next in Assembly Judiciary on July 3.

ENHANCEMENT OF ATTORNEY GENERAL ENFORCEMENT ACT: AB 1950 (Davis) to strengthen the law enforcement response to mortgage and foreclosure fraud.

v AB 1950: Passed out of Assembly (56-22). It passed out of Senate Banking (5-0) on June 27 and will be heard next in the Senate Judiciary, July 3, 2012.

ATTORNEY GENERAL SPECIAL GRAND JURY ACT: AB 1763 (Davis) and SB 1474 (Hancock) to strengthen prosecutions of complex, multi-jurisdictional fraud and crimes.

v SB 1474: Passed out of Senate (38-0). Passed out of Assembly Public Safety (4-0) and will be heard next in Assembly Appropriations.

v AB 1763: Passed out of Assembly (78-0). Passed out of Senate Public Safety on June 26 (7-0). It will be heard next in Senate Appropriations.

Assembly Bill No. 278

CHAPTER 86

An act to amend and add Sections 2923.5 and 2923.6 of, to amend and

repeal Section 2924 of, to add Sections 2920.5, 2923.4, 2923.7, 2924.17,

and 2924.20 to, to add and repeal Sections 2923.55, 2924.9, 2924.10,

2924.18, and 2924.19 of, and to add, repeal, and add Sections 2924.11,

2924.12, and 2924.15 of, the Civil Code, relating to mortgages.

[Approved by Governor July 11, 2012. Filed with

Secretary of State July 11, 2012.]

legislative counsel’s digest

AB 278, Eng. Mortgages and deeds of trust: foreclosure.

(1) Existing law, until January 1, 2013, requires a mortgagee, trustee,

beneficiary, or authorized agent to contact the borrower prior to filing a

notice of default to explore options for the borrower to avoid foreclosure,

as specified. Existing law requires a notice of default or, in certain

circumstances, a notice of sale, to include a declaration stating that the

mortgagee, trustee, beneficiary, or authorized agent has contacted the

borrower, or has tried with due diligence to contact the borrower, or that no

contact was required for a specified reason.

This bill would add mortgage servicers, as defined, to these provisions

and would extend the operation of these provisions indefinitely, except that

it would delete the requirement with respect to a notice of sale. The bill

would, until January 1, 2018, additionally require the borrower, as defined,

to be provided with specified information in writing prior to recordation of

a notice of default and, in certain circumstances, within 5 business days

after recordation. The bill would prohibit a mortgage servicer, mortgagee,

trustee, beneficiary, or authorized agent from recording a notice of default

or, until January 1, 2018, recording a notice of sale or conducting a trustee’s

sale while a complete first lien loan modification application is pending,

under specified conditions. The bill would, until January 1, 2018, establish

additional procedures to be followed regarding a first lien loan modification

application, the denial of an application, and a borrower’s right to appeal a

denial.

(2) Existing law imposes various requirements that must be satisfied

prior to exercising a power of sale under a mortgage or deed of trust,

including, among other things, recording a notice of default and a notice of

sale.

The bill would, until January 1, 2018, require a written notice to the

borrower after the postponement of a foreclosure sale in order to advise the

borrower of any new sale date and time, as specified. The bill would provide

that an entity shall not record a notice of default or otherwise initiate the

94

foreclosure process unless it is the holder of the beneficial interest under

the deed of trust, the original or substituted trustee, or the designated agent

of the holder of the beneficial interest, as specified.

The bill would prohibit recordation of a notice of default or a notice of

sale or the conduct of a trustee’s sale if a foreclosure prevention alternative

has been approved and certain conditions exist and would, until January 1,

2018, require recordation of a rescission of those notices upon execution of

a permanent foreclosure prevention alternative. The bill would, until January

1, 2018, prohibit the collection of application fees and the collection of late

fees while a foreclosure prevention alternative is being considered, if certain

criteria are met, and would require a subsequent mortgage servicer to honor

any previously approved foreclosure prevention alternative.

The bill would authorize a borrower to seek an injunction and damages

for violations of certain of the provisions described above, except as

specified. The bill would authorize the greater of treble actual damages or

$50,000 in statutory damages if a violation of certain provisions is found

to be intentional or reckless or resulted from willful misconduct, as specified.

The bill would authorize the awarding of attorneys’ fees for prevailing

borrowers, as specified. Violations of these provisions by licensees of the

Department of Corporations, the Department of Financial Institutions, and

the Department of Real Estate would also be violations of those respective

licensing laws. Because a violation of certain of those licensing laws is a

crime, the bill would impose a state-mandated local program.

The bill would provide that the requirements imposed on mortgage

servicers, and mortgagees, trustees, beneficiaries, and authorized agents,

described above are applicable only to mortgages or deeds of trust secured

by residential real property not exceeding 4 dwelling units that is

owner-occupied, as defined, and, until January 1, 2018, only to those entities

who conduct more than 175 foreclosure sales per year or annual reporting

period, except as specified.

The bill would require, upon request from a borrower who requests a

foreclosure prevention alternative, a mortgage servicer who conducts more

than 175 foreclosure sales per year or annual reporting period to establish

a single point of contact and provide the borrower with one or more direct

means of communication with the single point of contact. The bill would

specify various responsibilities of the single point of contact. The bill would

define single point of contact for these purposes.

(3) Existing law prescribes documents that may be recorded or filed in

court.

This bill would require that a specified declaration, notice of default,

notice of sale, deed of trust, assignment of a deed of trust, substitution of

trustee, or declaration or affidavit filed in any court relative to a foreclosure

proceeding or recorded by or on behalf of a mortgage servicer shall be

accurate and complete and supported by competent and reliable evidence.

The bill would require that before recording or filing any of those documents,

a mortgage servicer shall ensure that it has reviewed competent and reliable

evidence to substantiate the borrower’s default and the right to foreclose,

94

Ch. 86 — 2 —

including the borrower’s loan status and loan information. The bill would,

until January 1, 2018, provide that any mortgage servicer that engages in

multiple and repeated violations of these requirements shall be liable for a

civil penalty of up to $7,500 per mortgage or deed of trust, in an action

brought by specified state and local government entities, and would also

authorize administrative enforcement against licensees of the Department

of Corporations, the Department of Financial Institutions, and the Department

of Real Estate.

The bill would authorize the Department of Corporations, the Department

of Financial Institutions, and the Department of Real Estate to adopt

regulations applicable to persons and entities under their respective

jurisdictions for purposes of the provisions described above. The bill would

provide that a violation of those regulations would be enforceable only by

the regulating agency.

(4) The bill would state findings and declarations of the Legislature in

relation to foreclosures in the state generally, and would state the purposes

of the bill.

(5) The California Constitution requires the state to reimburse local

agencies and school districts for certain costs mandated by the state. Statutory

provisions establish procedures for making that reimbursement.

This bill would provide that no reimbursement is required by this act for

a specified reason.

The people of the State of California do enact as follows:

SECTION 1. The Legislature finds and declares all of the following:

(a) California is still reeling from the economic impacts of a wave of

residential property foreclosures that began in 2007. From 2007 to 2011

alone, there were over 900,000 completed foreclosure sales. In 2011, 38 of

the top 100 hardest hit ZIP Codes in the nation were in California, and the

current wave of foreclosures continues apace. All of this foreclosure activity

has adversely affected property values and resulted in less money for schools,

public safety, and other public services. In addition, according to the Urban

Institute, every foreclosure imposes significant costs on local governments,

including an estimated nineteen thousand two hundred twenty-nine dollars

($19,229) in local government costs. And the foreclosure crisis is not over;

there remain more than two million “underwater” mortgages in California.

(b) It is essential to the economic health of this state to mitigate the

negative effects on the state and local economies and the housing market

that are the result of continued foreclosures by modifying the foreclosure

process to ensure that borrowers who may qualify for a foreclosure

alternative are considered for, and have a meaningful opportunity to obtain,

available loss mitigation options. These changes to the state’s foreclosure

process are essential to ensure that the current crisis is not worsened by

unnecessarily adding foreclosed properties to the market when an alternative

to foreclosure may be available. Avoiding foreclosure, where possible, will

94

— 3 — Ch. 86

help stabilize the state’s housing market and avoid the substantial,

corresponding negative effects of foreclosures on families, communities,

and the state and local economy.

(c) This act is necessary to provide stability to California’s statewide and

regional economies and housing market by facilitating opportunities for

borrowers to pursue loss mitigation options.

SEC. 2. Section 2920.5 is added to the Civil Code, to read:

2920.5. For purposes of this article, the following definitions apply:

(a) “Mortgage servicer” means a person or entity who directly services

a loan, or who is responsible for interacting with the borrower, managing

the loan account on a daily basis including collecting and crediting periodic

loan payments, managing any escrow account, or enforcing the note and

security instrument, either as the current owner of the promissory note or

as the current owner’s authorized agent. “Mortgage servicer” also means a

subservicing agent to a master servicer by contract. “Mortgage servicer”

shall not include a trustee, or a trustee’s authorized agent, acting under a

power of sale pursuant to a deed of trust.

(b) “Foreclosure prevention alternative” means a first lien loan

modification or another available loss mitigation option.

(c) (1) Unless otherwise provided and for purposes of Sections 2923.4,

2923.5, 2923.55, 2923.6, 2923.7, 2924.9, 2924.10, 2924.11, 2924.18, and

2924.19, “borrower” means any natural person who is a mortgagor or trustor

and who is potentially eligible for any federal, state, or proprietary

foreclosure prevention alternative program offered by, or through, his or

her mortgage servicer.

(2) For purposes of the sections listed in paragraph (1), “borrower” shall

not include any of the following:

(A) An individual who has surrendered the secured property as evidenced

by either a letter confirming the surrender or delivery of the keys to the

property to the mortgagee, trustee, beneficiary, or authorized agent.

(B) An individual who has contracted with an organization, person, or

entity whose primary business is advising people who have decided to leave

their homes on how to extend the foreclosure process and avoid their

contractual obligations to mortgagees or beneficiaries.

(C) An individual who has filed a case under Chapter 7, 11, 12, or 13 of

Title 11 of the United States Code and the bankruptcy court has not entered

an order closing or dismissing the bankruptcy case, or granting relief from

a stay of foreclosure.

(d) “First lien” means the most senior mortgage or deed of trust on the

property that is the subject of the notice of default or notice of sale.

SEC. 3. Section 2923.4 is added to the Civil Code, to read:

2923.4. (a) The purpose of the act that added this section is to ensure

that, as part of the nonjudicial foreclosure process, borrowers are considered

for, and have a meaningful opportunity to obtain, available loss mitigation

options, if any, offered by or through the borrower’s mortgage servicer,

such as loan modifications or other alternatives to foreclosure. Nothing in

94

Ch. 86 — 4 —

the act that added this section, however, shall be interpreted to require a

particular result of that process.

(b) Nothing in this article obviates or supersedes the obligations of the

signatories to the consent judgment entered in the case entitled United States

of America et al. v. Bank of America Corporation et al., filed in the United

States District Court for the District of Columbia, case number

1:12-cv-00361 RMC.

SEC. 4. Section 2923.5 of the Civil Code is amended to read:

2923.5. (a) (1) A mortgage servicer, mortgagee, trustee, beneficiary,

or authorized agent may not record a notice of default pursuant to Section

2924 until both of the following:

(A) Either 30 days after initial contact is made as required by paragraph

(2) or 30 days after satisfying the due diligence requirements as described

in subdivision (e).

(B) The mortgage servicer complies with paragraph (1) of subdivision

(a) of Section 2924.18, if the borrower has provided a complete application

as defined in subdivision (d) of Section 2924.18.

(2) A mortgage servicer shall contact the borrower in person or by

telephone in order to assess the borrower’s financial situation and explore

options for the borrower to avoid foreclosure. During the initial contact, the

mortgage servicer shall advise the borrower that he or she has the right to

request a subsequent meeting and, if requested, the mortgage servicer shall

schedule the meeting to occur within 14 days. The assessment of the

borrower’s financial situation and discussion of options may occur during

the first contact, or at the subsequent meeting scheduled for that purpose.

In either case, the borrower shall be provided the toll-free telephone number

made available by the United States Department of Housing and Urban

Development (HUD) to find a HUD-certified housing counseling agency.

Any meeting may occur telephonically.

(b) A notice of default recorded pursuant to Section 2924 shall include

a declaration that the mortgage servicer has contacted the borrower, has

tried with due diligence to contact the borrower as required by this section,

or that no contact was required because the individual did not meet the

definition of “borrower” pursuant to subdivision (c) of Section 2920.5.

(c) A mortgage servicer’s loss mitigation personnel may participate by

telephone during any contact required by this section.

(d) A borrower may designate, with consent given in writing, a

HUD-certified housing counseling agency, attorney, or other adviser to

discuss with the mortgage servicer, on the borrower’s behalf, the borrower’s

financial situation and options for the borrower to avoid foreclosure. That

contact made at the direction of the borrower shall satisfy the contact

requirements of paragraph (2) of subdivision (a). Any loan modification or

workout plan offered at the meeting by the mortgage servicer is subject to

approval by the borrower.

(e) A notice of default may be recorded pursuant to Section 2924 when

a mortgage servicer has not contacted a borrower as required by paragraph

(2) of subdivision (a) provided that the failure to contact the borrower

94

— 5 — Ch. 86

occurred despite the due diligence of the mortgage servicer. For purposes

of this section, “due diligence” shall require and mean all of the following:

(1) A mortgage servicer shall first attempt to contact a borrower by

sending a first-class letter that includes the toll-free telephone number made

available by HUD to find a HUD-certified housing counseling agency.

(2) (A) After the letter has been sent, the mortgage servicer shall attempt

to contact the borrower by telephone at least three times at different hours

and on different days. Telephone calls shall be made to the primary telephone

number on file.

(B) A mortgage servicer may attempt to contact a borrower using an

automated system to dial borrowers, provided that, if the telephone call is

answered, the call is connected to a live representative of the mortgage

servicer.

(C) A mortgage servicer satisfies the telephone contact requirements of

this paragraph if it determines, after attempting contact pursuant to this

paragraph, that the borrower’s primary telephone number and secondary

telephone number or numbers on file, if any, have been disconnected.

(3) If the borrower does not respond within two weeks after the telephone

call requirements of paragraph (2) have been satisfied, the mortgage servicer

shall then send a certified letter, with return receipt requested.

(4) The mortgage servicer shall provide a means for the borrower to

contact it in a timely manner, including a toll-free telephone number that

will provide access to a live representative during business hours.

(5) The mortgage servicer has posted a prominent link on the homepage

of its Internet Web site, if any, to the following information:

(A) Options that may be available to borrowers who are unable to afford

their mortgage payments and who wish to avoid foreclosure, and instructions

to borrowers advising them on steps to take to explore those options.

(B) A list of financial documents borrowers should collect and be

prepared to present to the mortgage servicer when discussing options for

avoiding foreclosure.

(C) A toll-free telephone number for borrowers who wish to discuss

options for avoiding foreclosure with their mortgage servicer.

(D) The toll-free telephone number made available by HUD to find a

HUD-certified housing counseling agency.

(f) This section shall apply only to mortgages or deeds of trust described

in Section 2924.15.

(g) This section shall apply only to entities described in subdivision (b)

of Section 2924.18.

(h) This section shall remain in effect only until January 1, 2018, and as

of that date is repealed, unless a later enacted statute, that is enacted before

January 1, 2018, deletes or extends that date.

SEC. 5. Section 2923.5 is added to the Civil Code, to read:

2923.5. (a) (1) A mortgage servicer, mortgagee, trustee, beneficiary,

or authorized agent may not record a notice of default pursuant to Section

2924 until both of the following:

94

Ch. 86 — 6 —

(A) Either 30 days after initial contact is made as required by paragraph

(2) or 30 days after satisfying the due diligence requirements as described

in subdivision (e).

(B) The mortgage servicer complies with subdivision (a) of Section

2924.11, if the borrower has provided a complete application as defined in

subdivision (f) of Section 2924.11.

(2) A mortgage servicer shall contact the borrower in person or by

telephone in order to assess the borrower’s financial situation and explore

options for the borrower to avoid foreclosure. During the initial contact, the

mortgage servicer shall advise the borrower that he or she has the right to

request a subsequent meeting and, if requested, the mortgage servicer shall

schedule the meeting to occur within 14 days. The assessment of the

borrower’s financial situation and discussion of options may occur during

the first contact, or at the subsequent meeting scheduled for that purpose.

In either case, the borrower shall be provided the toll-free telephone number

made available by the United States Department of Housing and Urban

Development (HUD) to find a HUD-certified housing counseling agency.

Any meeting may occur telephonically.

(b) A notice of default recorded pursuant to Section 2924 shall include

a declaration that the mortgage servicer has contacted the borrower, has

tried with due diligence to contact the borrower as required by this section,

or that no contact was required because the individual did not meet the

definition of “borrower” pursuant to subdivision (c) of Section 2920.5.

(c) A mortgage servicer’s loss mitigation personnel may participate by

telephone during any contact required by this section.

(d) A borrower may designate, with consent given in writing, a

HUD-certified housing counseling agency, attorney, or other adviser to

discuss with the mortgage servicer, on the borrower’s behalf, the borrower’s

financial situation and options for the borrower to avoid foreclosure. That

contact made at the direction of the borrower shall satisfy the contact

requirements of paragraph (2) of subdivision (a). Any loan modification or

workout plan offered at the meeting by the mortgage servicer is subject to

approval by the borrower.

(e) A notice of default may be recorded pursuant to Section 2924 when

a mortgage servicer has not contacted a borrower as required by paragraph

(2) of subdivision (a) provided that the failure to contact the borrower

occurred despite the due diligence of the mortgage servicer. For purposes

of this section, “due diligence” shall require and mean all of the following:

(1) A mortgage servicer shall first attempt to contact a borrower by

sending a first-class letter that includes the toll-free telephone number made

available by HUD to find a HUD-certified housing counseling agency.

(2) (A) After the letter has been sent, the mortgage servicer shall attempt

to contact the borrower by telephone at least three times at different hours

and on different days. Telephone calls shall be made to the primary telephone

number on file.

(B) A mortgage servicer may attempt to contact a borrower using an

automated system to dial borrowers, provided that, if the telephone call is

94

— 7 — Ch. 86

answered, the call is connected to a live representative of the mortgage

servicer.

(C) A mortgage servicer satisfies the telephone contact requirements of

this paragraph if it determines, after attempting contact pursuant to this

paragraph, that the borrower’s primary telephone number and secondary

telephone number or numbers on file, if any, have been disconnected.

(3) If the borrower does not respond within two weeks after the telephone

call requirements of paragraph (2) have been satisfied, the mortgage servicer

shall then send a certified letter, with return receipt requested.

(4) The mortgage servicer shall provide a means for the borrower to

contact it in a timely manner, including a toll-free telephone number that

will provide access to a live representative during business hours.

(5) The mortgage servicer has posted a prominent link on the homepage

of its Internet Web site, if any, to the following information:

(A) Options that may be available to borrowers who are unable to afford

their mortgage payments and who wish to avoid foreclosure, and instructions

to borrowers advising them on steps to take to explore those options.

(B) A list of financial documents borrowers should collect and be

prepared to present to the mortgage servicer when discussing options for

avoiding foreclosure.

(C) A toll-free telephone number for borrowers who wish to discuss

options for avoiding foreclosure with their mortgage servicer.

(D) The toll-free telephone number made available by HUD to find a

HUD-certified housing counseling agency.

(f) This section shall apply only to mortgages or deeds of trust described

in Section 2924.15.

(g) This section shall become operative on January 1, 2018.

SEC. 6. Section 2923.55 is added to the Civil Code, to read:

2923.55. (a) A mortgage servicer, mortgagee, trustee, beneficiary, or

authorized agent may not record a notice of default pursuant to Section 2924

until all of the following:

(1) The mortgage servicer has satisfied the requirements of paragraph

(1) of subdivision (b).

(2) Either 30 days after initial contact is made as required by paragraph

(2) of subdivision (b) or 30 days after satisfying the due diligence

requirements as described in subdivision (f).

(3) The mortgage servicer complies with subdivision (c) of Section

2923.6, if the borrower has provided a complete application as defined in

subdivision (h) of Section 2923.6.

(b) (1) As specified in subdivision (a), a mortgage servicer shall send

the following information in writing to the borrower:

(A) A statement that if the borrower is a servicemember or a dependent

of a servicemember, he or she may be entitled to certain protections under

the federal Servicemembers Civil Relief Act (50 U.S.C. Sec. 501 et seq.)

regarding the servicemember’s interest rate and the risk of foreclosure, and

counseling for covered servicemembers that is available at agencies such

as Military OneSource and Armed Forces Legal Assistance.

94

Ch. 86 — 8 —

(B) A statement that the borrower may request the following:

(i) A copy of the borrower’s promissory note or other evidence of

indebtedness.

(ii) A copy of the borrower’s deed of trust or mortgage.

(iii) A copy of any assignment, if applicable, of the borrower’s mortgage

or deed of trust required to demonstrate the right of the mortgage servicer

to foreclose.

(iv) A copy of the borrower’s payment history since the borrower was

last less than 60 days past due.

(2) A mortgage servicer shall contact the borrower in person or by

telephone in order to assess the borrower’s financial situation and explore

options for the borrower to avoid foreclosure. During the initial contact, the

mortgage servicer shall advise the borrower that he or she has the right to

request a subsequent meeting and, if requested, the mortgage servicer shall

schedule the meeting to occur within 14 days. The assessment of the

borrower’s financial situation and discussion of options may occur during

the first contact, or at the subsequent meeting scheduled for that purpose.

In either case, the borrower shall be provided the toll-free telephone number

made available by the United States Department of Housing and Urban

Development (HUD) to find a HUD-certified housing counseling agency.

Any meeting may occur telephonically.

(c) A notice of default recorded pursuant to Section 2924 shall include

a declaration that the mortgage servicer has contacted the borrower, has

tried with due diligence to contact the borrower as required by this section,

or that no contact was required because the individual did not meet the

definition of “borrower” pursuant to subdivision (c) of Section 2920.5.

(d) A mortgage servicer’s loss mitigation personnel may participate by

telephone during any contact required by this section.

(e) A borrower may designate, with consent given in writing, a

HUD-certified housing counseling agency, attorney, or other adviser to

discuss with the mortgage servicer, on the borrower’s behalf, the borrower’s

financial situation and options for the borrower to avoid foreclosure. That

contact made at the direction of the borrower shall satisfy the contact

requirements of paragraph (2) of subdivision (b). Any foreclosure prevention

alternative offered at the meeting by the mortgage servicer is subject to

approval by the borrower.

(f) A notice of default may be recorded pursuant to Section 2924 when

a mortgage servicer has not contacted a borrower as required by paragraph

(2) of subdivision (b), provided that the failure to contact the borrower

occurred despite the due diligence of the mortgage servicer. For purposes

of this section, “due diligence” shall require and mean all of the following:

(1) A mortgage servicer shall first attempt to contact a borrower by

sending a first-class letter that includes the toll-free telephone number made

available by HUD to find a HUD-certified housing counseling agency.

(2) (A) After the letter has been sent, the mortgage servicer shall attempt

to contact the borrower by telephone at least three times at different hours

94

— 9 — Ch. 86

and on different days. Telephone calls shall be made to the primary telephone

number on file.

(B) A mortgage servicer may attempt to contact a borrower using an

automated system to dial borrowers, provided that, if the telephone call is

answered, the call is connected to a live representative of the mortgage

servicer.

(C) A mortgage servicer satisfies the telephone contact requirements of

this paragraph if it determines, after attempting contact pursuant to this

paragraph, that the borrower’s primary telephone number and secondary

telephone number or numbers on file, if any, have been disconnected.

(3) If the borrower does not respond within two weeks after the telephone

call requirements of paragraph (2) have been satisfied, the mortgage servicer

shall then send a certified letter, with return receipt requested, that includes

the toll-free telephone number made available by HUD to find a

HUD-certified housing counseling agency.

(4) The mortgage servicer shall provide a means for the borrower to

contact it in a timely manner, including a toll-free telephone number that

will provide access to a live representative during business hours.

(5) The mortgage servicer has posted a prominent link on the homepage

of its Internet Web site, if any, to the following information:

(A) Options that may be available to borrowers who are unable to afford

their mortgage payments and who wish to avoid foreclosure, and instructions

to borrowers advising them on steps to take to explore those options.

(B) A list of financial documents borrowers should collect and be

prepared to present to the mortgage servicer when discussing options for

avoiding foreclosure.

(C) A toll-free telephone number for borrowers who wish to discuss

options for avoiding foreclosure with their mortgage servicer.

(D) The toll-free telephone number made available by HUD to find a

HUD-certified housing counseling agency.

(g) This section shall not apply to entities described in subdivision (b)

of Section 2924.18.

(h) This section shall apply only to mortgages or deeds of trust described

in Section 2924.15.

(i) This section shall remain in effect only until January 1, 2018, and as

of that date is repealed, unless a later enacted statute, that is enacted before

January 1, 2018, deletes or extends that date.

SEC. 7. Section 2923.6 of the Civil Code is amended to read:

2923.6. (a) The Legislature finds and declares that any duty that

mortgage servicers may have to maximize net present value under their

pooling and servicing agreements is owed to all parties in a loan pool, or to

all investors under a pooling and servicing agreement, not to any particular

party in the loan pool or investor under a pooling and servicing agreement,

and that a mortgage servicer acts in the best interests of all parties to the

loan pool or investors in the pooling and servicing agreement if it agrees to

or implements a loan modification or workout plan for which both of the

following apply:

94

Ch. 86 — 10 —

(1) The loan is in payment default, or payment default is reasonably

foreseeable.

(2) Anticipated recovery under the loan modification or workout plan

exceeds the anticipated recovery through foreclosure on a net present value

basis.

(b) It is the intent of the Legislature that the mortgage servicer offer the

borrower a loan modification or workout plan if such a modification or plan

is consistent with its contractual or other authority.

(c) If a borrower submits a complete application for a first lien loan

modification offered by, or through, the borrower’s mortgage servicer, a

mortgage servicer, mortgagee, trustee, beneficiary, or authorized agent shall

not record a notice of default or notice of sale, or conduct a trustee’s sale,

while the complete first lien loan modification application is pending. A

mortgage servicer, mortgagee, trustee, beneficiary, or authorized agent shall

not record a notice of default or notice of sale or conduct a trustee’s sale

until any of the following occurs:

(1) The mortgage servicer makes a written determination that the borrower

is not eligible for a first lien loan modification, and any appeal period

pursuant to subdivision (d) has expired.

(2) The borrower does not accept an offered first lien loan modification

within 14 days of the offer.

(3) The borrower accepts a written first lien loan modification, but

defaults on, or otherwise breaches the borrower’s obligations under, the

first lien loan modification.

(d) If the borrower’s application for a first lien loan modification is

denied, the borrower shall have at least 30 days from the date of the written

denial to appeal the denial and to provide evidence that the mortgage

servicer’s determination was in error.

(e) If the borrower’s application for a first lien loan modification is

denied, the mortgage servicer, mortgagee, trustee, beneficiary, or authorized

agent shall not record a notice of default or, if a notice of default has already

been recorded, record a notice of sale or conduct a trustee’s sale until the

later of:

(1) Thirty-one days after the borrower is notified in writing of the denial.

(2) If the borrower appeals the denial pursuant to subdivision (d), the

later of 15 days after the denial of the appeal or 14 days after a first lien

loan modification is offered after appeal but declined by the borrower, or,

if a first lien loan modification is offered and accepted after appeal, the date

on which the borrower fails to timely submit the first payment or otherwise

breaches the terms of the offer.

(f) Following the denial of a first lien loan modification application, the

mortgage servicer shall send a written notice to the borrower identifying

the reasons for denial, including the following:

(1) The amount of time from the date of the denial letter in which the

borrower may request an appeal of the denial of the first lien loan

modification and instructions regarding how to appeal the denial.

94

— 11 — Ch. 86

(2) If the denial was based on investor disallowance, the specific reasons

for the investor disallowance.

(3) If the denial is the result of a net present value calculation, the monthly

gross income and property value used to calculate the net present value and

a statement that the borrower may obtain all of the inputs used in the net

present value calculation upon written request to the mortgage servicer.

(4) If applicable, a finding that the borrower was previously offered a

first lien loan modification and failed to successfully make payments under

the terms of the modified loan.

(5) If applicable, a description of other foreclosure prevention alternatives

for which the borrower may be eligible, and a list of the steps the borrower

must take in order to be considered for those options. If the mortgage servicer

has already approved the borrower for another foreclosure prevention

alternative, information necessary to complete the foreclosure prevention

alternative.

(g) In order to minimize the risk of borrowers submitting multiple

applications for first lien loan modifications for the purpose of delay, the

mortgage servicer shall not be obligated to evaluate applications from

borrowers who have already been evaluated or afforded a fair opportunity

to be evaluated for a first lien loan modification prior to January 1, 2013,

or who have been evaluated or afforded a fair opportunity to be evaluated

consistent with the requirements of this section, unless there has been a

material change in the borrower’s financial circumstances since the date of

the borrower’s previous application and that change is documented by the

borrower and submitted to the mortgage servicer.

(h) For purposes of this section, an application shall be deemed

“complete” when a borrower has supplied the mortgage servicer with all

documents required by the mortgage servicer within the reasonable

timeframes specified by the mortgage servicer.

(i) Subdivisions (c) to (h), inclusive, shall not apply to entities described

in subdivision (b) of Section 2924.18.

(j) This section shall apply only to mortgages or deeds of trust described

in Section 2924.15.

(k) This section shall remain in effect only until January 1, 2018, and

as of that date is repealed, unless a later enacted statute, that is enacted

before January 1, 2018, deletes or extends that date.

SEC. 8. Section 2923.6 is added to the Civil Code, to read:

2923.6. (a) The Legislature finds and declares that any duty mortgage

servicers may have to maximize net present value under their pooling and

servicing agreements is owed to all parties in a loan pool, or to all investors

under a pooling and servicing agreement, not to any particular party in the

loan pool or investor under a pooling and servicing agreement, and that a

mortgage servicer acts in the best interests of all parties to the loan pool or

investors in the pooling and servicing agreement if it agrees to or implements

a loan modification or workout plan for which both of the following apply:

(1) The loan is in payment default, or payment default is reasonably

foreseeable.

94

Ch. 86 — 12 —

(2) Anticipated recovery under the loan modification or workout plan

exceeds the anticipated recovery through foreclosure on a net present value

basis.

(b) It is the intent of the Legislature that the mortgage servicer offer the

borrower a loan modification or workout plan if such a modification or plan

is consistent with its contractual or other authority.

(c) This section shall become operative on January 1, 2018.

SEC. 9. Section 2923.7 is added to the Civil Code, to read:

2923.7. (a) Upon request from a borrower who requests a foreclosure

prevention alternative, the mortgage servicer shall promptly establish a

single point of contact and provide to the borrower one or more direct means

of communication with the single point of contact.

(b) The single point of contact shall be responsible for doing all of the

following:

(1) Communicating the process by which a borrower may apply for an

available foreclosure prevention alternative and the deadline for any required

submissions to be considered for these options.

(2) Coordinating receipt of all documents associated with available

foreclosure prevention alternatives and notifying the borrower of any missing

documents necessary to complete the application.

(3) Having access to current information and personnel sufficient to

timely, accurately, and adequately inform the borrower of the current status

of the foreclosure prevention alternative.

(4) Ensuring that a borrower is considered for all foreclosure prevention

alternatives offered by, or through, the mortgage servicer, if any.

(5) Having access to individuals with the ability and authority to stop

foreclosure proceedings when necessary.

(c) The single point of contact shall remain assigned to the borrower’s

account until the mortgage servicer determines that all loss mitigation options

offered by, or through, the mortgage servicer have been exhausted or the

borrower’s account becomes current.

(d) The mortgage servicer shall ensure that a single point of contact refers

and transfers a borrower to an appropriate supervisor upon request of the

borrower, if the single point of contact has a supervisor.

(e) For purposes of this section, “single point of contact” means an

individual or team of personnel each of whom has the ability and authority

to perform the responsibilities described in subdivisions (b) to (d), inclusive.

The mortgage servicer shall ensure that each member of the team is

knowledgeable about the borrower’s situation and current status in the

alternatives to foreclosure process.

(f) This section shall apply only to mortgages or deeds of trust described

in Section 2924.15.

(g) (1) This section shall not apply to a depository institution chartered

under state or federal law, a person licensed pursuant to Division 9

(commencing with Section 22000) or Division 20 (commencing with Section

50000) of the Financial Code, or a person licensed pursuant to Part 1

(commencing with Section 10000) of Division 4 of the Business and

94

— 13 — Ch. 86

Professions Code, that, during its immediately preceding annual reporting

period, as established with its primary regulator, foreclosed on 175 or fewer

residential real properties, containing no more than four dwelling units, that

are located in California.

(2) Within three months after the close of any calendar year or annual

reporting period as established with its primary regulator during which an

entity or person described in paragraph (1) exceeds the threshold of 175

specified in paragraph (1), that entity shall notify its primary regulator, in

a manner acceptable to its primary regulator, and any mortgagor or trustor

who is delinquent on a residential mortgage loan serviced by that entity of

the date on which that entity will be subject to this section, which date shall

be the first day of the first month that is six months after the close of the

calendar year or annual reporting period during which that entity exceeded

the threshold.

SEC. 10. Section 2924 of the Civil Code, as amended by Section 1 of

Chapter 180 of the Statutes of 2010, is amended to read:

2924. (a) Every transfer of an interest in property, other than in trust,

made only as a security for the performance of another act, is to be deemed

a mortgage, except when in the case of personal property it is accompanied

by actual change of possession, in which case it is to be deemed a pledge.

Where, by a mortgage created after July 27, 1917, of any estate in real

property, other than an estate at will or for years, less than two, or in any

transfer in trust made after July 27, 1917, of a like estate to secure the

performance of an obligation, a power of sale is conferred upon the

mortgagee, trustee, or any other person, to be exercised after a breach of

the obligation for which that mortgage or transfer is a security, the power

shall not be exercised except where the mortgage or transfer is made pursuant

to an order, judgment, or decree of a court of record, or to secure the payment

of bonds or other evidences of indebtedness authorized or permitted to be

issued by the Commissioner of Corporations, or is made by a public utility

subject to the provisions of the Public Utilities Act, until all of the following

apply:

(1) The trustee, mortgagee, or beneficiary, or any of their authorized

agents shall first file for record, in the office of the recorder of each county

wherein the mortgaged or trust property or some part or parcel thereof is

situated, a notice of default. That notice of default shall include all of the

following:

(A) A statement identifying the mortgage or deed of trust by stating the

name or names of the trustor or trustors and giving the book and page, or

instrument number, if applicable, where the mortgage or deed of trust is

recorded or a description of the mortgaged or trust property.

(B) A statement that a breach of the obligation for which the mortgage

or transfer in trust is security has occurred.

(C) A statement setting forth the nature of each breach actually known

to the beneficiary and of his or her election to sell or cause to be sold the

property to satisfy that obligation and any other obligation secured by the

deed of trust or mortgage that is in default.

94

Ch. 86 — 14 —

(D) If the default is curable pursuant to Section 2924c, the statement

specified in paragraph (1) of subdivision (b) of Section 2924c.

(2) Not less than three months shall elapse from the filing of the notice

of default.

(3) Except as provided in paragraph (4), after the lapse of the three months

described in paragraph (2), the mortgagee, trustee, or other person authorized

to take the sale shall give notice of sale, stating the time and place thereof,

in the manner and for a time not less than that set forth in Section 2924f.

(4) Notwithstanding paragraph (3), the mortgagee, trustee, or other person

authorized to take sale may record a notice of sale pursuant to Section 2924f

up to five days before the lapse of the three-month period described in

paragraph (2), provided that the date of sale is no earlier than three months

and 20 days after the recording of the notice of default.

(5) Until January 1, 2018, whenever a sale is postponed for a period of

at least 10 business days pursuant to Section 2924g, a mortgagee, beneficiary,

or authorized agent shall provide written notice to a borrower regarding the

new sale date and time, within five business days following the

postponement. Information provided pursuant to this paragraph shall not

constitute the public declaration required by subdivision (d) of Section

2924g. Failure to comply with this paragraph shall not invalidate any sale

that would otherwise be valid under Section 2924f. This paragraph shall be

inoperative on January 1, 2018.

(6) No entity shall record or cause a notice of default to be recorded or

otherwise initiate the foreclosure process unless it is the holder of the

beneficial interest under the mortgage or deed of trust, the original trustee

or the substituted trustee under the deed of trust, or the designated agent of

the holder of the beneficial interest. No agent of the holder of the beneficial

interest under the mortgage or deed of trust, original trustee or substituted

trustee under the deed of trust may record a notice of default or otherwise

commence the foreclosure process except when acting within the scope of

authority designated by the holder of the beneficial interest.

(b) In performing acts required by this article, the trustee shall incur no

liability for any good faith error resulting from reliance on information

provided in good faith by the beneficiary regarding the nature and the amount

of the default under the secured obligation, deed of trust, or mortgage. In

performing the acts required by this article, a trustee shall not be subject to

Title 1.6c (commencing with Section 1788) of Part 4.

(c) A recital in the deed executed pursuant to the power of sale of

compliance with all requirements of law regarding the mailing of copies of

notices or the publication of a copy of the notice of default or the personal

delivery of the copy of the notice of default or the posting of copies of the

notice of sale or the publication of a copy thereof shall constitute prima

facie evidence of compliance with these requirements and conclusive

evidence thereof in favor of bona fide purchasers and encumbrancers for

value and without notice.

(d) All of the following shall constitute privileged communications

pursuant to Section 47:

94

— 15 — Ch. 86

(1) The mailing, publication, and delivery of notices as required by this

section.

(2) Performance of the procedures set forth in this article.

(3) Performance of the functions and procedures set forth in this article

if those functions and procedures are necessary to carry out the duties

described in Sections 729.040, 729.050, and 729.080 of the Code of Civil

Procedure.

(e) There is a rebuttable presumption that the beneficiary actually knew

of all unpaid loan payments on the obligation owed to the beneficiary and

secured by the deed of trust or mortgage subject to the notice of default.

However, the failure to include an actually known default shall not invalidate

the notice of sale and the beneficiary shall not be precluded from asserting

a claim to this omitted default or defaults in a separate notice of default.

SEC. 11. Section 2924 of the Civil Code, as amended by Section 2 of

Chapter 180 of the Statutes of 2010, is repealed.

SEC. 12. Section 2924.9 is added to the Civil Code, to read:

2924.9. (a) Unless a borrower has previously exhausted the first lien

loan modification process offered by, or through, his or her mortgage servicer

described in Section 2923.6, within five business days after recording a

notice of default pursuant to Section 2924, a mortgage servicer that offers

one or more foreclosure prevention alternatives shall send a written

communication to the borrower that includes all of the following information:

(1) That the borrower may be evaluated for a foreclosure prevention

alternative or, if applicable, foreclosure prevention alternatives.

(2) Whether an application is required to be submitted by the borrower

in order to be considered for a foreclosure prevention alternative.

(3) The means and process by which a borrower may obtain an application

for a foreclosure prevention alternative.

(b) This section shall not apply to entities described in subdivision (b)

of Section 2924.18.

(c) This section shall apply only to mortgages or deeds of trust described

in Section 2924.15.

(d) This section shall remain in effect only until January 1, 2018, and

as of that date is repealed, unless a later enacted statute, that is enacted

before January 1, 2018, deletes or extends that date.

SEC. 13. Section 2924.10 is added to the Civil Code, to read:

2924.10. (a) When a borrower submits a complete first lien modification

application or any document in connection with a first lien modification

application, the mortgage servicer shall provide written acknowledgment

of the receipt of the documentation within five business days of receipt. In

its initial acknowledgment of receipt of the loan modification application,

the mortgage servicer shall include the following information:

(1) A description of the loan modification process, including an estimate

of when a decision on the loan modification will be made after a complete

application has been submitted by the borrower and the length of time the

borrower will have to consider an offer of a loan modification or other

foreclosure prevention alternative.

94

Ch. 86 — 16 —

(2) Any deadlines, including deadlines to submit missing documentation,

that would affect the processing of a first lien loan modification application.

(3) Any expiration dates for submitted documents.

(4) Any deficiency in the borrower’s first lien loan modification

application.

(b) For purposes of this section, a borrower’s first lien loan modification

application shall be deemed to be “complete” when a borrower has supplied

the mortgage servicer with all documents required by the mortgage servicer

within the reasonable timeframes specified by the mortgage servicer.

(c) This section shall not apply to entities described in subdivision (b)

of Section 2924.18.

(d) This section shall apply only to mortgages or deeds of trust described

in Section 2924.15.

(e) This section shall remain in effect only until January 1, 2018, and

as of that date is repealed, unless a later enacted statute, that is enacted

before January 1, 2018, deletes or extends that date.

SEC. 14. Section 2924.11 is added to the Civil Code, to read:

2924.11. (a) If a foreclosure prevention alternative is approved in writing

prior to the recordation of a notice of default, a mortgage servicer, mortgagee,

trustee, beneficiary, or authorized agent shall not record a notice of default

under either of the following circumstances:

(1) The borrower is in compliance with the terms of a written trial or

permanent loan modification, forbearance, or repayment plan.

(2) A foreclosure prevention alternative has been approved in writing by

all parties, including, for example, the first lien investor, junior lienholder,

and mortgage insurer, as applicable, and proof of funds or financing has

been provided to the servicer.

(b) If a foreclosure prevention alternative is approved in writing after

the recordation of a notice of default, a mortgage servicer, mortgagee, trustee,

beneficiary, or authorized agent shall not record a notice of sale or conduct

a trustee’s sale under either of the following circumstances:

(1) The borrower is in compliance with the terms of a written trial or

permanent loan modification, forbearance, or repayment plan.

(2) A foreclosure prevention alternative has been approved in writing by

all parties, including, for example, the first lien investor, junior lienholder,

and mortgage insurer, as applicable, and proof of funds or financing has

been provided to the servicer.

(c) When a borrower accepts an offered first lien loan modification or

other foreclosure prevention alternative, the mortgage servicer shall provide

the borrower with a copy of the fully executed loan modification agreement

or agreement evidencing the foreclosure prevention alternative following

receipt of the executed copy from the borrower.

(d) A mortgagee, beneficiary, or authorized agent shall record a rescission

of a notice of default or cancel a pending trustee’s sale, if applicable, upon

the borrower executing a permanent foreclosure prevention alternative. In

the case of a short sale, the rescission or cancellation of the pending trustee’s

sale shall occur when the short sale has been approved by all parties and

94

— 17 — Ch. 86

proof of funds or financing has been provided to the mortgagee, beneficiary,

or authorized agent.

(e) The mortgage servicer shall not charge any application, processing,

or other fee for a first lien loan modification or other foreclosure prevention

alternative.

(f) The mortgage servicer shall not collect any late fees for periods during

which a complete first lien loan modification application is under

consideration or a denial is being appealed, the borrower is making timely

modification payments, or a foreclosure prevention alternative is being

evaluated or exercised.

(g) If a borrower has been approved in writing for a first lien loan

modification or other foreclosure prevention alternative, and the servicing

of that borrower’s loan is transferred or sold to another mortgage servicer,

the subsequent mortgage servicer shall continue to honor any previously

approved first lien loan modification or other foreclosure prevention

alternative, in accordance with the provisions of the act that added this

section.

(h) This section shall apply only to mortgages or deeds of trust described

in Section 2924.15.

(i) This section shall not apply to entities described in subdivision (b) of

Section 2924.18.

(j) This section shall remain in effect only until January 1, 2018, and as

of that date is repealed, unless a later enacted statute, that is enacted before

January 1, 2018, deletes or extends that date.

SEC. 15. Section 2924.11 is added to the Civil Code, to read:

2924.11. (a) If a borrower submits a complete application for a

foreclosure prevention alternative offered by, or through, the borrower’s

mortgage servicer, a mortgage servicer, trustee, mortgagee, beneficiary, or

authorized agent shall not record a notice of sale or conduct a trustee’s sale

while the complete foreclosure prevention alternative application is pending,

and until the borrower has been provided with a written determination by

the mortgage servicer regarding that borrower’s eligibility for the requested

foreclosure prevention alternative.

(b) Following the denial of a first lien loan modification application, the

mortgage servicer shall send a written notice to the borrower identifying

with specificity the reasons for the denial and shall include a statement that

the borrower may obtain additional documentation supporting the denial

decision upon written request to the mortgage servicer.

(c) If a foreclosure prevention alternative is approved in writing prior to

the recordation of a notice of default, a mortgage servicer, mortgagee, trustee,

beneficiary, or authorized agent shall not record a notice of default under

either of the following circumstances:

(1) The borrower is in compliance with the terms of a written trial or

permanent loan modification, forbearance, or repayment plan.

(2) A foreclosure prevention alternative has been approved in writing by

all parties, including, for example, the first lien investor, junior lienholder,

94

Ch. 86 — 18 —

and mortgage insurer, as applicable, and proof of funds or financing has

been provided to the servicer.

(d) If a foreclosure prevention alternative is approved in writing after

the recordation of a notice of default, a mortgage servicer, mortgagee, trustee,

beneficiary, or authorized agent shall not record a notice of sale or conduct

a trustee’s sale under either of the following circumstances:

(1) The borrower is in compliance with the terms of a written trial or

permanent loan modification, forbearance, or repayment plan.

(2) A foreclosure prevention alternative has been approved in writing by

all parties, including, for example, the first lien investor, junior lienholder,

and mortgage insurer, as applicable, and proof of funds or financing has

been provided to the servicer.

(e) This section applies only to mortgages or deeds of trust as described

in Section 2924.15.

(f) For purposes of this section, an application shall be deemed “complete”

when a borrower has supplied the mortgage servicer with all documents

required by the mortgage servicer within the reasonable timeframes specified

by the mortgage servicer.

(g) This section shall become operative on January 1, 2018.

SEC. 16. Section 2924.12 is added to the Civil Code, to read:

2924.12. (a) (1) If a trustee’s deed upon sale has not been recorded, a

borrower may bring an action for injunctive relief to enjoin a material

violation of Section 2923.55, 2923.6, 2923.7, 2924.9, 2924.10, 2924.11, or

2924.17.

(2) Any injunction shall remain in place and any trustee’s sale shall be

enjoined until the court determines that the mortgage servicer, mortgagee,

trustee, beneficiary, or authorized agent has corrected and remedied the

violation or violations giving rise to the action for injunctive relief. An

enjoined entity may move to dissolve an injunction based on a showing that

the material violation has been corrected and remedied.

(b) After a trustee’s deed upon sale has been recorded, a mortgage

servicer, mortgagee, trustee, beneficiary, or authorized agent shall be liable

to a borrower for actual economic damages pursuant to Section 3281,

resulting from a material violation of Section 2923.55, 2923.6, 2923.7,

2924.9, 2924.10, 2924.11, or 2924.17 by that mortgage servicer, mortgagee,

trustee, beneficiary, or authorized agent where the violation was not corrected

and remedied prior to the recordation of the trustee’s deed upon sale. If the

court finds that the material violation was intentional or reckless, or resulted

from willful misconduct by a mortgage servicer, mortgagee, trustee,

beneficiary, or authorized agent, the court may award the borrower the

greater of treble actual damages or statutory damages of fifty thousand

dollars ($50,000).

(c) A mortgage servicer, mortgagee, trustee, beneficiary, or authorized

agent shall not be liable for any violation that it has corrected and remedied

prior to the recordation of a trustee’s deed upon sale, or that has been

corrected and remedied by third parties working on its behalf prior to the

recordation of a trustee’s deed upon sale.

94

— 19 — Ch. 86

(d) A violation of Section 2923.55, 2923.6, 2923.7, 2924.9, 2924.10,

2924.11, or 2924.17 by a person licensed by the Department of Corporations,

Department of Financial Institutions, or Department of Real Estate shall be

deemed to be a violation of that person’s licensing law.

(e) No violation of this article shall affect the validity of a sale in favor

of a bona fide purchaser and any of its encumbrancers for value without

notice.

(f) A third-party encumbrancer shall not be relieved of liability resulting

from violations of Section 2923.55, 2923.6, 2923.7, 2924.9, 2924.10,

2924.11, or 2924.17 committed by that third-party encumbrancer, that

occurred prior to the sale of the subject property to the bona fide purchaser.

(g) A signatory to a consent judgment entered in the case entitled United

States of America et al. v. Bank of America Corporation et al., filed in the

United States District Court for the District of Columbia, case number

1:12-cv-00361 RMC, that is in compliance with the relevant terms of the

Settlement Term Sheet of that consent judgment with respect to the borrower

who brought an action pursuant to this section while the consent judgment

is in effect shall have no liability for a violation of Section 2923.55, 2923.6,

2923.7, 2924.9, 2924.10, 2924.11, or 2924.17.

(h) The rights, remedies, and procedures provided by this section are in

addition to and independent of any other rights, remedies, or procedures

under any other law. Nothing in this section shall be construed to alter, limit,

or negate any other rights, remedies, or procedures provided by law.

(i) A court may award a prevailing borrower reasonable attorney’s fees

and costs in an action brought pursuant to this section. A borrower shall be

deemed to have prevailed for purposes of this subdivision if the borrower

obtained injunctive relief or was awarded damages pursuant to this section.

(j) This section shall not apply to entities described in subdivision (b) of

Section 2924.18.

(k) This section shall remain in effect only until January 1, 2018, and

as of that date is repealed, unless a later enacted statute, that is enacted

before January 1, 2018, deletes or extends that date.

SEC. 17. Section 2924.12 is added to the Civil Code, to read:

2924.12. (a) (1) If a trustee’s deed upon sale has not been recorded, a

borrower may bring an action for injunctive relief to enjoin a material

violation of Section 2923.5, 2923.7, 2924.11, or 2924.17.

(2) Any injunction shall remain in place and any trustee’s sale shall be

enjoined until the court determines that the mortgage servicer, mortgagee,

trustee, beneficiary, or authorized agent has corrected and remedied the

violation or violations giving rise to the action for injunctive relief. An

enjoined entity may move to dissolve an injunction based on a showing that

the material violation has been corrected and remedied.

(b) After a trustee’s deed upon sale has been recorded, a mortgage

servicer, mortgagee, trustee, beneficiary, or authorized agent shall be liable

to a borrower for actual economic damages pursuant to Section 3281,

resulting from a material violation of Section 2923.5, 2923.7, 2924.11, or

2924.17 by that mortgage servicer, mortgagee, trustee, beneficiary, or

94

Ch. 86 — 20 —

authorized agent where the violation was not corrected and remedied prior

to the recordation of the trustee’s deed upon sale. If the court finds that the

material violation was intentional or reckless, or resulted from willful

misconduct by a mortgage servicer, mortgagee, trustee, beneficiary, or

authorized agent, the court may award the borrower the greater of treble

actual damages or statutory damages of fifty thousand dollars ($50,000).

(c) A mortgage servicer, mortgagee, trustee, beneficiary, or authorized

agent shall not be liable for any violation that it has corrected and remedied

prior to the recordation of the trustee’s deed upon sale, or that has been

corrected and remedied by third parties working on its behalf prior to the

recordation of the trustee’s deed upon sale.

(d) A violation of Section 2923.5, 2923.7, 2924.11, or 2924.17 by a

person licensed by the Department of Corporations, Department of Financial

Institutions, or Department of Real Estate shall be deemed to be a violation

of that person’s licensing law.

(e) No violation of this article shall affect the validity of a sale in favor

of a bona fide purchaser and any of its encumbrancers for value without

notice.

(f) A third-party encumbrancer shall not be relieved of liability resulting

from violations of Section 2923.5, 2923.7, 2924.11, or 2924.17 committed

by that third-party encumbrancer, that occurred prior to the sale of the subject

property to the bona fide purchaser.

(g) The rights, remedies, and procedures provided by this section are in

addition to and independent of any other rights, remedies, or procedures

under any other law. Nothing in this section shall be construed to alter, limit,

or negate any other rights, remedies, or procedures provided by law.

(h) A court may award a prevailing borrower reasonable attorney’s fees

and costs in an action brought pursuant to this section. A borrower shall be

deemed to have prevailed for purposes of this subdivision if the borrower

obtained injunctive relief or was awarded damages pursuant to this section.

(i) This section shall become operative on January 1, 2018.

SEC. 18. Section 2924.15 is added to the Civil Code, to read:

2924.15. (a) Unless otherwise provided, paragraph (5) of subdivision

(a) of Section 2924, and Sections 2923.5, 2923.55, 2923.6, 2923.7, 2924.9,

2924.10, 2924.11, and 2924.18 shall apply only to first lien mortgages or

deeds of trust that are secured by owner-occupied residential real property

containing no more than four dwelling units. For these purposes,

“owner-occupied” means that the property is the principal residence of the

borrower and is security for a loan made for personal, family, or household

purposes.

(b) This section shall remain in effect only until January 1, 2018, and

as of that date is repealed, unless a later enacted statute, that is enacted

before January 1, 2018, deletes or extends that date.

SEC. 19. Section 2924.15 is added to the Civil Code, to read:

2924.15. (a) Unless otherwise provided, Sections 2923.5, 2923.7, and

2924.11 shall apply only to first lien mortgages or deeds of trust that are

secured by owner-occupied residential real property containing no more

94

— 21 — Ch. 86

than four dwelling units. For these purposes, “owner-occupied” means that

the property is the principal residence of the borrower and is security for a

loan made for personal, family, or household purposes.

(b) This section shall become operative on January 1, 2018.

SEC. 20. Section 2924.17 is added to the Civil Code, to read:

2924.17. (a) A declaration recorded pursuant to Section 2923.5 or, until

January 1, 2018, pursuant to Section 2923.55, a notice of default, notice of

sale, assignment of a deed of trust, or substitution of trustee recorded by or

on behalf of a mortgage servicer in connection with a foreclosure subject

to the requirements of Section 2924, or a declaration or affidavit filed in

any court relative to a foreclosure proceeding shall be accurate and complete

and supported by competent and reliable evidence.

(b) Before recording or filing any of the documents described in

subdivision (a), a mortgage servicer shall ensure that it has reviewed

competent and reliable evidence to substantiate the borrower’s default and

the right to foreclose, including the borrower’s loan status and loan

information.

(c) Until January 1, 2018, any mortgage servicer that engages in multiple

and repeated uncorrected violations of subdivision (b) in recording

documents or filing documents in any court relative to a foreclosure

proceeding shall be liable for a civil penalty of up to seven thousand five

hundred dollars ($7,500) per mortgage or deed of trust in an action brought

by a government entity identified in Section 17204 of the Business and

Professions Code, or in an administrative proceeding brought by the

Department of Corporations, the Department of Real Estate, or the

Department of Financial Institutions against a respective licensee, in addition

to any other remedies available to these entities. This subdivision shall be

inoperative on January 1, 2018.

SEC. 21. Section 2924.18 is added to the Civil Code, to read:

2924.18. (a) (1) If a borrower submits a complete application for a first

lien loan modification offered by, or through, the borrower’s mortgage

servicer, a mortgage servicer, trustee, mortgagee, beneficiary, or authorized

agent shall not record a notice of default, notice of sale, or conduct a trustee’s

sale while the complete first lien loan modification application is pending,

and until the borrower has been provided with a written determination by

the mortgage servicer regarding that borrower’s eligibility for the requested

loan modification.

(2) If a foreclosure prevention alternative has been approved in writing

prior to the recordation of a notice of default, a mortgage servicer, mortgagee,

trustee, beneficiary, or authorized agent shall not record a notice of default

under either of the following circumstances:

(A) The borrower is in compliance with the terms of a written trial or

permanent loan modification, forbearance, or repayment plan.

(B) A foreclosure prevention alternative has been approved in writing

by all parties, including, for example, the first lien investor, junior lienholder,

and mortgage insurer, as applicable, and proof of funds or financing has

been provided to the servicer.

94

Ch. 86 — 22 —

(3) If a foreclosure prevention alternative is approved in writing after

the recordation of a notice of default, a mortgage servicer, mortgagee, trustee,

beneficiary, or authorized agent shall not record a notice of sale or conduct

a trustee’s sale under either of the following circumstances:

(A) The borrower is in compliance with the terms of a written trial or

permanent loan modification, forbearance, or repayment plan.

(B) A foreclosure prevention alternative has been approved in writing

by all parties, including, for example, the first lien investor, junior lienholder,

and mortgage insurer, as applicable, and proof of funds or financing has

been provided to the servicer.

(b) This section shall apply only to a depository institution chartered

under state or federal law, a person licensed pursuant to Division 9